To inflate or not to inflate? That is the question. ~ Jerome H. (Hamlet) Powell

The principal issue in the

eccentric world of macroeconomic policy-making focuses on inflation, as my currently-germane

alteration of Hamlet’s famous soliloquy states above. Is it rising and staying

for a while or is it merely a temporary drive-by event?

Even though a great deal depends on it, no one knows the answer. That’s despite economists’ reviewing decades of data and using their forecasting models day and night. That hasn’t stopped specialists from offering many differing opinions; following the adage, “often wrong, but never in doubt.” Perhaps macroeconomists should add trendspotting algorithms that have become popular in the fashion industry into their models.

For economists, inflation refers

to an increase in the overall level of a nation’s prices. More technically,

inflation occurs when aggregate prices of consumer goods and services rise due

to “excessive” demand or insufficient supply. As prices rise, the purchasing

value of money consequently falls.

Aggregate prices is a nebulous

macroeconomic concept referring to a measure of prices for all of our

nation’s final goods and services– from soap to syringes, and everything

in-between, like Buicks, donuts and urologist visits. Our most-often used

measure of inflation is the Consumer Price Index (CPI) that is calculated

monthly by the Labor Department’s Bureau of Labor Statistics (BLS).

The CPI offers quite a few

different “flavors” of prices, like prices for urban consumers, for urban wage

earners and for the elderly. The BLS gathers data on consumer prices for each

of 211 different categories of consumer items (the “market basket” of goods and

services) in 38 different geographical areas throughout the US.

When the BLS released the May CPI

information on June 10, the media and others took serious note. During the last

12 months, the CPI increased 5.0%, the largest 12-month increase since August

2008. This annualized increase is over two times as large as the 2% inflation

rate that Mr. Powell, Chair of Federal Reserve Bank, hopes to see.

At the Fed’s summer meetings last

week, officials stated they would keep interest rates near zero, but explicitly

stated they would consider increasing rates, perhaps twice by the end of 2023

if inflation persists. This statement is a direct reaction to the May CPI

announcement. 2023 is a year sooner than the Fed has previously stated for considering

interest rate changes. The Fed thus has increased inflationary expectations.

Unsurprisingly, stock markets took that news poorly, dropping almost one

percent and bond yields increased.

The Fed steadfastly maintains

that current inflation is “transitory,” never defining what that term means. The

last two months have presented higher-than-expected annualized inflation, 4.2%

in April, 5.0% in May. If June’s CPI number is 4% or greater. it will be much

harder for the Fed to proclaim again it is transitory. We’ll know on July 13.

The Fed’s transitory belief rests

on two premises. First, aggregate production will continue to increase steadily

as recent parts shortages and supply-chain lags ameliorate, like chip-sets for autos

and trucks and lumber for construction. Second, consumers’ demand for goods and

services now reflects surging needs that were restricted during the extended

covid period; these will taper. Thus, after this temporary phase, markets will

get back to “more normal” behavior with more goods and services available and

less pent-up demand.

Most importantly, policy-makers need to adopt a more farsighted view of our economic activities, which is vital for producing well-founded economic programs. Monthly CPI data are interesting and instructive, just as weekly unemployment claims requests are. But these very short-term data are inherently quite variable. Their use should not be overemphasized, as they seemed to have become. Most economists are far better at drilling down for detailed information than we are at looking up. Adopting a broader, longer-term perspective will produce stronger, fairer policies.

The media have filled screens,

airwaves and newsprint with stories about how May’s unexpectedly large CPI reflected

price increases in specific slices of the economy. A Washington Post story

mentioned consumers are paying more for an array of products, including bacon and

used Buicks, as the economy rebounds strongly from the brief covid-led

recession.

Several items whose prices have

notably risen include used cars (Buicks and beyond), furniture, gasoline,

washing machines and dryers, bicycles, lumber and airfare. Beef and

non-Congressional pork prices have also risen.

But not to worry spending-fans.

In January, House Dems after a decade-long ban, resurrected personal earmarked

projects. These “pork” projects can be specifically-funded by a single

Congressperson that circumvent the standard merit-based and competitive

allocation process. How can you be upset at this change? There’s a $1.4

trillion per year limit for such projects. The Dems insist these pork-rind

earmarks will provide lawmakers new tools to better serve their communities,

and bring home the higher-priced bacon. Praise be? Not.

Back to Buicks. The mention of

old Buicks immediately recalled my grandfather’s, which looked much like the

one shown below. When we visited, he drove us in his sweet midnight-black,

side-portholed Buick on fine Sunday rides through Western Massachusetts countryside.

They don’t build them like that anymore.

A 1951 Buick Special cost $1,800,

which in today’s dollars is $18,637. The 2021 Buick Encore, the lowest-priced

model like the Special, costs $26,260. That’s fair amount of auto inflation, to

the tune of $7,623 more than the CPI-adjusted Special price. This 41% premium

accounts in part for the vast increases in Buicks’ automotive quality and

technical improvements gained by GM over the past 70 years.

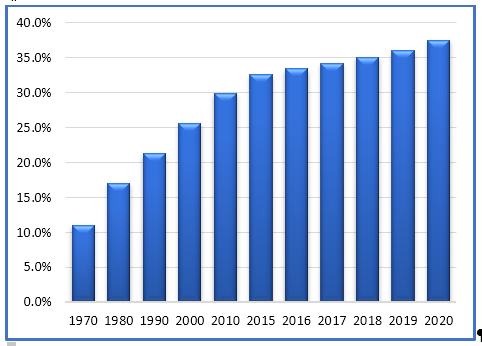

Our inflation rates have steadily fallen during the last 50 years, as shown in this table. The average

|

Decade |

Average Yearly Inflation Rate |

|

1971-80 |

7.86% |

|

1981-90 |

4.74% |

|

1991-2000 |

2.81% |

|

2001-10 |

2.38% |

|

2011-20 |

1.73% |

|

Source: DOL/BLS |

|

After 1982, US annual inflation has

never been greater than 5.4%. Thus, any American younger than 40 years old

would think high inflation was more than 5%, at worst. Long gone are the nasty macroeconomic

mid-1970s and early 1980s, when inflation never got below 5.7%.

The most recent decade’s average

inflation rate was 1.73%, thankfully less than one-quarter the 1970s level. The

FFR currently remains a rock-bottom 0.06%, unemployment has been steadily dropping

since April 2020, now is 5.8%.

Although people remain concerned

about inflation, US price increases are far smaller than a several other

countries. Venezuela’s citizens have faced the world’s worst inflation for

years due to massive government malfeasance. Last years’ inflation in Venezuela

was a gigantic 9,568%, down from a stratospheric 1,698,488% in 2018. Venezuela’s

cumulative inflation from 2016 to early 2019 was estimated at 53,798,500%. This

unfathomable inflation is the reason Venezuela’s official minimum monthly

wage is currently worth only $3.20. Zimbabwe, always high in international

rankings, has the second-topmost inflation at 767%. Such giant hyperinflation rates

are usually caused by the government’s oversized increase in the money supply

that cannot be warranted by (absent) economic growth.

Meanwhile back in Washington, Dems

in Congress continue wrestling with how to fund the administration’s expansive infrastructure

programs. Fearing that their more moderate colleagues’ nascent, bipartisan $1

trillion (T) effort will ignore many of their priorities, progressive Dems’

latest idea is to combine all their sprawling hopes into one single, giant

effort, perhaps as large as $6T – a wish-list including most Prog favorites. The

combined $7T possible infrastructure spending would represent 33% of our

current GDP. No matter how worthy such outlays might be, they would likely

unleash intimidating inflationary pressures.

Each of these bills face formidable

odds of passing in no small part because they will require every Senate Dem to

vote for them. Approving a single, $6T bill for widely-demarcated

infrastructure will push way beyond Senate prospects. One other hindrance is Congress’

feeble work schedule. House members plan to toil in Washington only 9 days

between now and Labor Day; Senators just 16 days. The House will not be in

session at any time in August. Legislative life on Capitol Hill is indeed very

different from other workplaces. Does such a schedule justify why we taxpayers

provide these “legislators” with a perhaps-inflated $174,000 salary?